A good proportion of us shy away at the mention of the word ‘maths’, but in the investing world there are some quirky mathematical outcomes that are worth reminding ourselves of. The first is that if an investment goes up 100% it only has to go down 50% to get back to where it started. The second is that if an investment goes down 50% it has to go back up 100% to get back to where it started. To some that may be obvious, but to others less so.

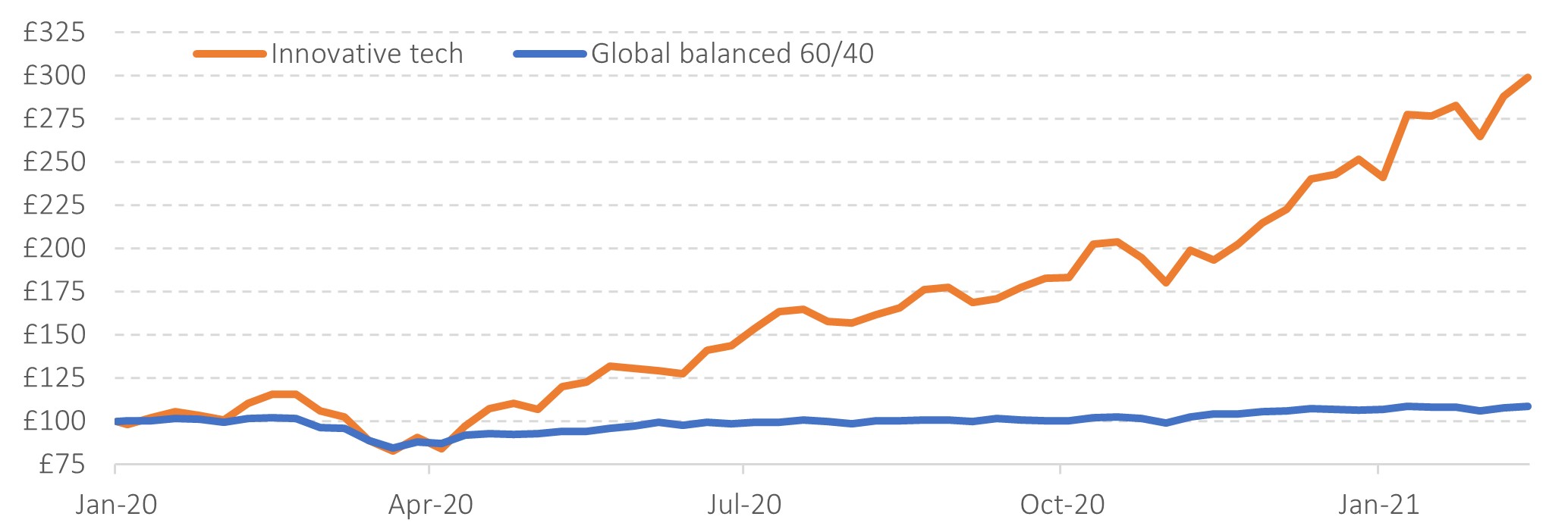

The past two years have given us quite a few live examples of this maths in action, including Cathy Woods’ innovative technology fund ARKK, which posted a stellar return of around 200% from the start of 2020 to February 2021. She quickly became the darling of the US financial TV shows. If we compare that to a more ‘boring’ portfolio comprising 60% in global equities and 40% in higher quality bonds[1], which returned in the region of 8% over the same period, we may feel a bit disappointed. Yet 8% is actually a good outcome, given that in Q1 2020 the markets fell substantially on the back of the pandemic.

Figure 1: ‘Peak’ ARKK (1 Jan 2020 to 21 Feb 2021)

Data: ARKK ETF and Global balanced 60% equity/40% bonds (see endnote) both in GBP.

If we roll on from the ‘peak’ of ARKK to 12 March 2022, we can see the asymmetry in percentage returns in action. ARKK has lost over 60% and is now almost back to where it started the period, despite its 200% rise.

Figure 1: ‘Peak’ ARKK (1 Jan 2020 to 21 Feb 2021)

Data: ARKK ETF and Global balanced 60% equity/40% bonds (see endnote) both in GBP.

Over the whole period, ARKK is up 13% and the global balanced portfolio is up 9%, so not much to choose between the two, or is there? There are two sides to the investment coin. One is return and the other is risk. Over the whole period, the ARKK fund is almost four times more volatile than the global balanced fund, which makes it inherently harder to live with.

The other useful lesson to take from this example is that most of the stellar performance occurred when the ARKK fund was relatively small. The 200% performance quoted above assumes that a lump sum was invested on 1st January 2020 and held for the period under review. Yet the fund only became popular once the bulk of the rise had already happened. A large component of investors’ money was invested at, or near, ‘peak’ ARKK and has suffered the bulk of the subsequent fall. Morningstar – a reputable, independent fund research house – has estimated[2] that in the three years to 31 December 2021, the total return (relating to a lump sum invested at the start of the period, otherwise known as a time-weighted return) was around 35% per annum (in USD terms). On the other hand, if fund flows are accounted for, the average investor generated a return somewhere in the region of 10% p.a. (known as the investor, or money-weighted, return). This 25% or so annual difference is sometimes referred to as the ‘behaviour gap’.

Sometimes the tortoise investor can feel left behind, but the diversified nature of their portfolio across markets, sectors, companies and other asset classes such as bonds, results in a much smoother journey to their destination. The highs may not be so high but the lows take less recovering from, reigning in the hare investor. This encourages tortoise investors to stay invested.

The maths of percentages in investment returns may be quirky, but it is important.

[1] The Vanguard Lifestrategy 60 Acc in GBP fund has been used for illustrative purposes only. This is not a recommendation – see endnote.

[2] www.morningstar.com/articles/1071658/arkk-an-object-lesson-in-how-not-to-invest. Accessed 17-03-2022

Risk warnings

This article is distributed for educational purposes and should not be considered investment advice or an offer of any security for sale. This article contains the opinions of the author but not necessarily the Firm and does not represent a recommendation of any particular security, strategy, or investment product. Information contained herein has been obtained from sources believed to be reliable but is not guaranteed.

Past performance is not indicative of future results and no representation is made that the stated results will be replicated.

![]()

About the author

Albion Strategic

Albion were born in 2001 and initially focused on working with private banks and family offices in the US. In 2006, it began consulting to leading financial planning companies in the UK, many of which have grown into robust, successful and respected firms with strong regional brands.

In that same year, Smarter Investing was published and is now in its third edition. Their systematic approach to investing was tested in the Credit Crisis of 2008-9 and survived with honours. The Albion approach has also been shown to be robust in the more positive markets since, capturing the bulk of returns offered by the markets.

Theory, evidence, logic and patience are the key ingredients to investing success.