Investors sometimes convince themselves that they know what the future holds and seek to position their portfolio to benefit from that knowledge. As one of our clients, you will know that this is not a game we play when it comes to investing money in your portfolio.

A topical example is the belief that central banks around the world must be about to raise their base rates – the rates that they pay commercial banks who lend them money – to combat rising inflation and meet their targets. The theory is that higher interest rates are passed through the economy and end investors are encouraged to save rather than to spend, reducing the impact of inflation[1]. Central bankers, however, will be the first to admit that this task is more difficult than it sounds!

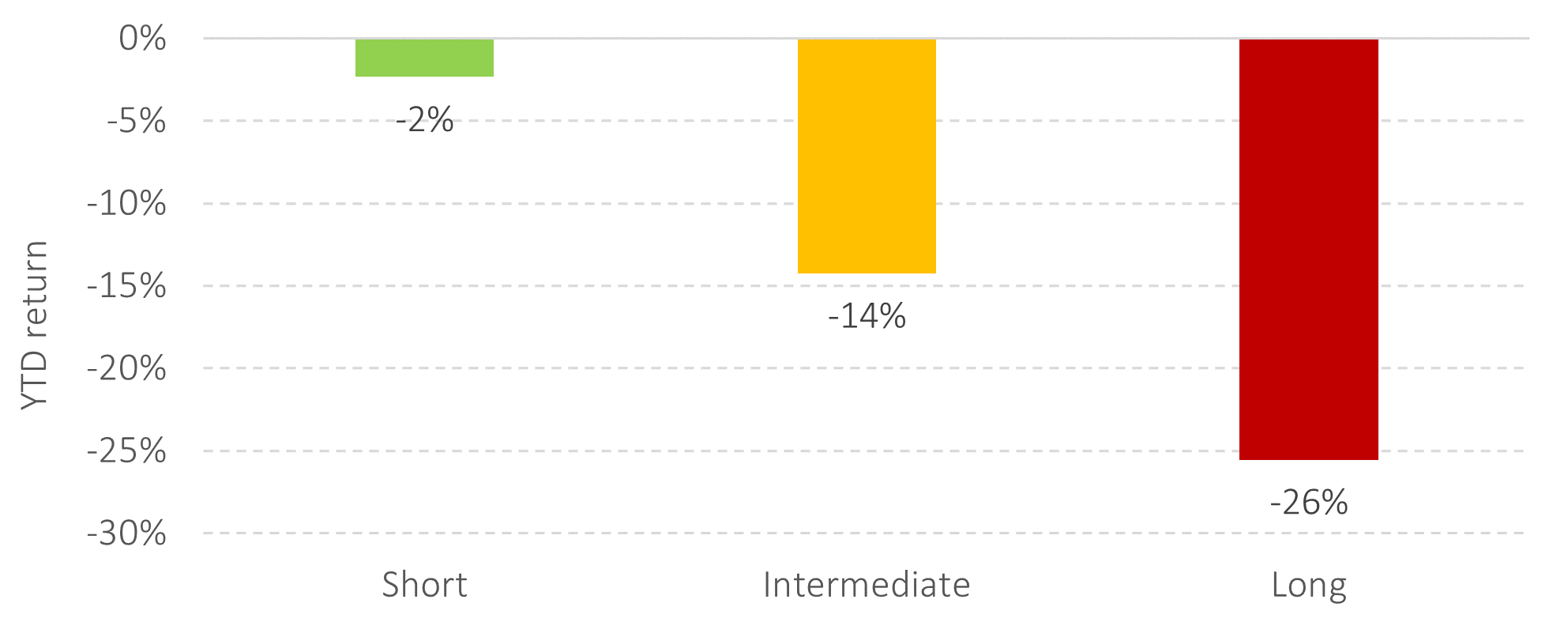

One thing we do know is that when interest rates in the bond market rise, outstanding bond prices fall to adjust to the more favourable market conditions. Put differently, older bonds were issued at lower interest rates and the market now pays a higher rate of interest. As a result, the older bonds are less desirable to own and their price falls in line with the new market yield. So far in 2022, bond markets have suffered price falls not seen for many years. It is some comfort that sticking to a shorter-dated strategy has mitigated the falls in your defensive assets. This has always been one of the risks for investors who choose to lend for longer.

Figure 1: UK government bond YTD performance by maturity (GBP)

Fund performance: L&G UK Gilt 0-5 Year ETF, iShares UK Gilts All Stocks, iShares Over 15 Years Gilts. YTD to 18/07/22.

What about the future? If a hypothetical tactical investor thought that the Bank of England was going to raise its base rate, which is currently 1.25%, to say 2% by the end of the year, they might expect bond prices to suffer further falls as this change is made and passed through to commercial banks – if interest rates rise, prices must fall. In a situation whereby this hypothetical investor’s view became the market consensus, the investor needs to have reached this conclusion, and acted on it, before other investors do, otherwise the opportunity gets arbitraged away. In a situation whereby it is not the market consensus, the hypothetical investor is betting against all other well-informed investors with opposing views. Even without reviewing market data this sounds like a tough game to win (and it is).

Bond investors know about base rates; they also know that central banks use them as a tool to try to control inflation. Therefore, the market already has an expectation of what the future base rate will be, which is reflected in current bond prices. Implied future base rates (i.e. the market’s expectation) can be derived from current prices: in mid-June this sat at 2.9% by the end of 2022 reaching 3.3% in 2023[2]. Some investors will have a lower projection, others will have a higher one, and the market sits at the aggregate of all investors.

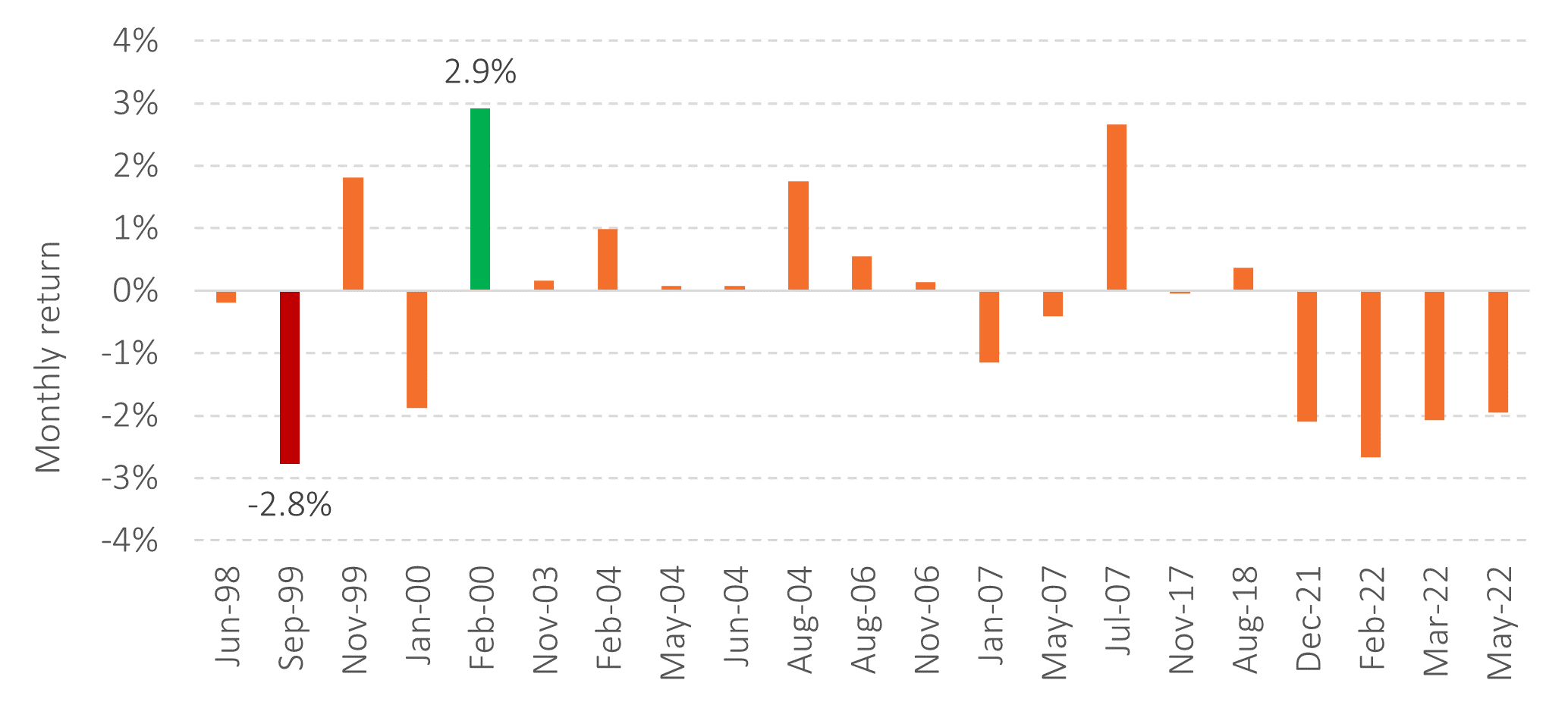

The reality is that prices adjust to new expectations due to the, by definition, random release of new information that we experience each and every day. The chart below shows that since 1998, UK government bond returns have actually been positive in 11 of the 21 months when the Bank of England raised base rates. Not only do tactical investors need to be able to predict an uncertain future, but they also need to be able to work out how all other investors will react to that future. Without a crystal ball, this is fool’s errand.

Figure 2: UK Gilt returns during months with base rate rises

Fund performance: Scottish Widows UK Fixed Income Tracker. Apr-98 to Jun-22.

Why is this important? It is important because accepting the market does a pretty good job at pricing information is a far more robust philosophy than trying to second guess it.

Over longer periods of time (15-20 years), around 80-90% of active managers are beaten by a sensible benchmark[3] across asset classes and geographies. If you thought of it, chances are so did the market and you would be best served to hold the faith in your strategy – keep calm and carry on.

‘Everybody has some information. The function of the markets is to aggregate that information, evaluate it and get it incorporated into prices.’

– Merton Miller, Ph.D., Nobel Laureate in Economics, 1990

[1] Bank of England (2022) Interest rates and Bank Rate. Target = 2%. https://www.bankofengland.co.uk/

[2] Bank of England (2022) Minutes of the Monetary Policy Committee Meeting – 16//06/22.

[3] S&P (2022) SPIVA Europe Scorecard – year-end 2021. https://www.spglobal.com/

Risk warnings

This article is distributed for educational purposes and should not be considered investment advice or an offer of any security for sale. This article contains the opinions of the author but not necessarily the Firm and does not represent a recommendation of any particular security, strategy, or investment product. Information contained herein has been obtained from sources believed to be reliable but is not guaranteed.

Past performance is not indicative of future results and no representation is made that the stated results will be replicated.

About the author

Albion Strategic

Albion were born in 2001 and initially focused on working with private banks and family offices in the US. In 2006, it began consulting to leading financial planning companies in the UK, many of which have grown into robust, successful and respected firms with strong regional brands.

In that same year, Smarter Investing was published and is now in its third edition. Their systematic approach to investing was tested in the Credit Crisis of 2008-9 and survived with honours. The Albion approach has also been shown to be robust in the more positive markets since, capturing the bulk of returns offered by the markets.

Theory, evidence, logic and patience are the key ingredients to investing success.