Most investors would probably like to forget the poor performance of both bonds and equities in 2022 and early 2023. For many investors it was their first real experience of bonds falling in value, particularly at the same time as equities. Different investors would have experienced different outcomes in 2022 (and subsequently) depending on the type of bonds that they held. It is worth revisiting what has happened since then.

Going back to first principles, we can remind ourselves of several characteristics that apply to bonds: Bond prices move in the opposite direction to bond yields i.e. when bond yields rise, bond prices fall; the prices of bonds with maturities further into the future are more sensitive to changes in yields than shorter-maturity bonds, making their prices more volatile; the lower the quality of the borrower issuing the bonds, the more like equities they behave; and finally, bond markets do not like inflation, generally driving up yields in the face of rising inflation.

In 2022, with the growing threat of high inflation following Russia’s invasion of Ukraine, exacerbated by the instability of the unfunded tax promises of the Conservative government under Liz Truss, bond yields rose dramatically and substantially.

The bond see-saw moved violently, with those owning longer-dated bonds suffering material and painful falls in value. Those who owned shorter-dated bonds fared better, but even so delivered falls in value. Yet, bond owners from that point on began to benefit from the higher yields that their bonds now delivered, recouping some of those falls in value.

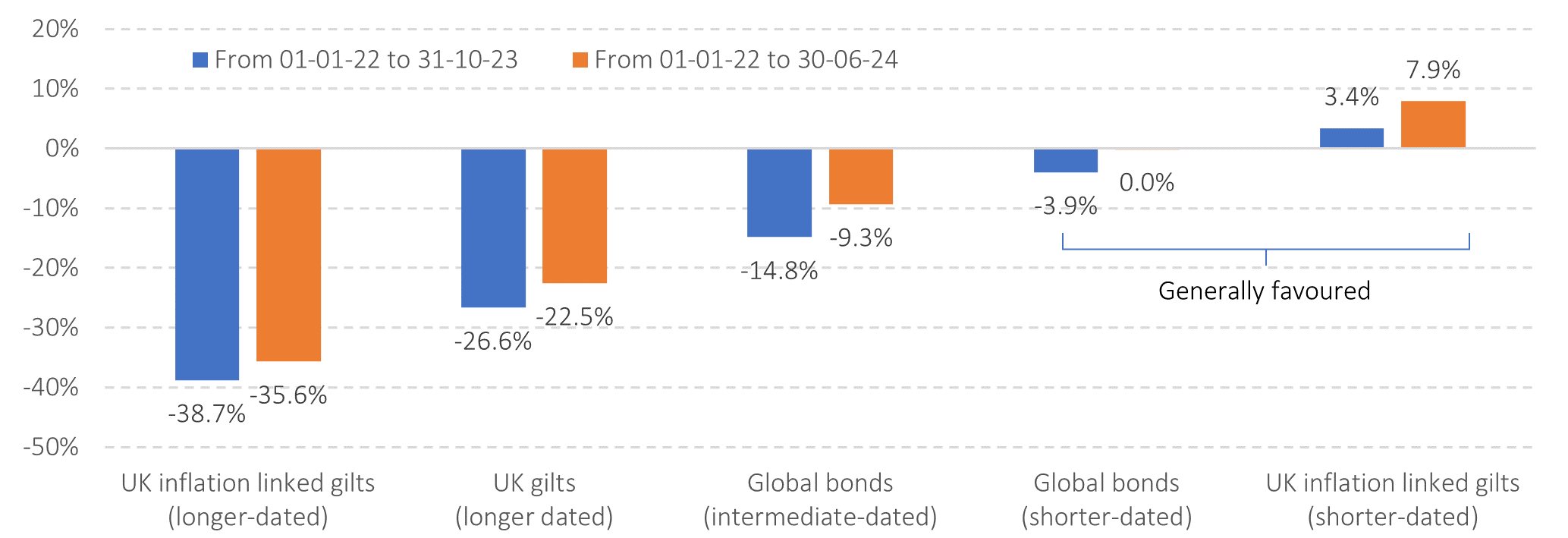

Take a look at the chart below which shows how far bonds fell for different maturities and what the return has been in cumulative terms since the start of the fall. As one can see, a big bond bounce-back for shorter-dated bonds has occurred, back to where they started, while longer-dated bonds still sit deeply underwater.

Figure 1: Bond falls and recoveries vary depending on what you own

Source: Morningstar Direct © All rights reserved – see endnote for details.

It is evident that shorter-dated bonds have recovered far more quickly than longer-dated bonds as the prices of the former fell less far, and the consequent higher yields have helped to recoup these falls, at least in nominal, pre-inflation terms. At their worst, shorter-dated global bonds were down around -7% in 2022. However, they delivered just over +5% in 2023, and around +1% to the end of June this year following small yield rises across major markets.

We have always tended to favour shorter-dated bonds for this reason believing that the small premium available in lending for longer is outweighed by the downside protection that comes from owning shorter-dated bonds alongside their bounce-back-ability!

Risk warnings

This article is distributed for educational purposes only and should not be considered investment advice or an offer of any security for sale. This article contains the opinions of the author but not necessarily the Firm and does not represent a recommendation of any particular security, strategy, or investment product. Reference to specific products is made only to help make educational points and does not constitute any form or recommendation or advice. Information contained herein has been obtained from sources believed to be reliable but is not guaranteed.

Past performance is not indicative of future results and no representation is made that the stated results will be replicated.

Use of Morningstar Direct© data

© Morningstar 2024. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied, adapted or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information, except where such damages or losses cannot be limited or excluded by law in your jurisdiction. Past financial performance is no guarantee of future results.

Data series used:

| Instrument | Asset class proxy |

| L&G All Stocks Index Linked Gilt Idx Tr, GB00B84QXT94 | UK inflation linked gilts (longer-dated) |

| L&G All Stocks Gilt Index Trust, GB00B8344798 | UK gilts (longer dated) |

| Vanguard Global Bd Idx, IE00B50W2R13 | Global bonds (intermediate-dated) |

| Vanguard Global S/T Bd Idx, IE00BH65QG55 | Global bonds (shorter-dated) |

| Albion Constant Maturity Bond Index (3Y, real) | UK inflation linked gilts (shorter-dated) |

About the author

Albion Strategic

Albion were born in 2001 and initially focused on working with private banks and family offices in the US. In 2006, they began consulting to leading financial planning companies in the UK, many of which have grown into robust, successful and respected firms with strong regional brands.

In that same year, Smarter Investing was published and is now in its third edition. Their systematic approach to investing was tested in the Credit Crisis of 2008-9 and survived with honours. The Albion approach has also been shown to be robust in the more positive markets since, capturing the bulk of returns offered by the markets.

Theory, evidence, logic and patience are the key ingredients to investing success.

Article image: https://bit.ly/4dkpBNo